Summary

There is now a growing need for broadband Internet access. The majority of subscribers are served through terrestrial (cable) or mobile networks; however, the deployment of terrestrial networks is not economically feasible for remote or sparsely populated areas. Broadband satellite communications are the only available solution for such areas. The main advantage of satellite Internet is the ubiquitous availability of Internet access (to circumpolar regions, as regards GEO satellites). GEO satellites are used with a view to providing broadband communication, but, in recent years, a number of companies have emerged, which are to this end planning to deploy large constellations of LEO/MEO satellites.

Satellite Internet has a number of disadvantages:

- High cost of services and subscriber equipment.

- Circumpolar regions are not covered (applies only to GEO SV).

- Signal latency associated with great distances (for GEO satellites).

- Decrease in the signal and its complete absence in a situation when the Sun and a satellite are in line with the receiving antenna (the Sun behind the satellite position). Typical for GEO satellites.

- Exposure to moisture and various forms of precipitation (especially when using Ka-band and Ku-band).

- There are usually throughput limitations (or limitations on the allowed volume of data per month).

The number of subscribers to satellite broadband is expected to grow steadily. In this regard, the North American region will be in the lead (in terms of the number of subscribers), and the Asia region will show the greatest growth. The programs of state funding of broadband (satellite) communications access for the areas not covered by terrestrial networks have been launched in the EU countries and the USA. The estimated broadband Internet market is about 433+ million households, and the current Satcom market penetration is only 0.63%, which is equivalent to 2.7 million consumers (of which 2 million are in the USA and served by two top players, EchoStar and ViaSat).

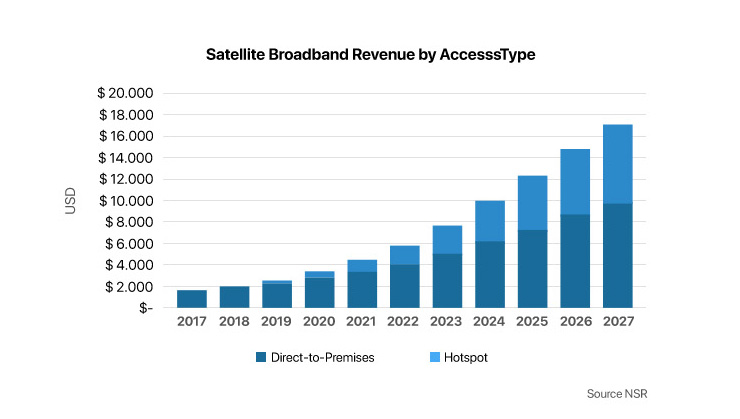

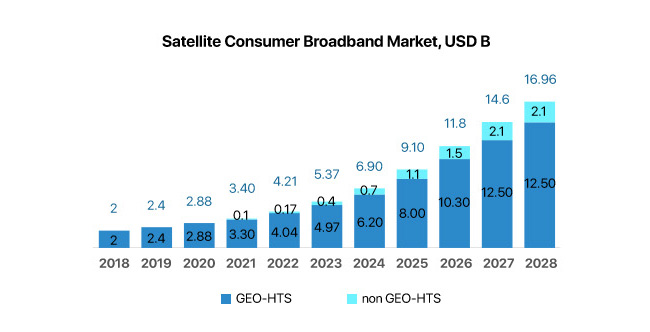

The broadband communications market is one of the Satcom market segments. This market is growing and is forecast (for the period of 2018 – 2028) to reach a total volume of USD 189B (revenue from services and equipment). In general, and in terms of end users, the market is divided into two large sectors: Enterprise VSAT and Consumer Broadband. The Consumer Broadband segment is USD 90.8B (total revenue for 2018 – 2028 including services and equipment), and the total revenue from services in the segment is expected to be USD 79.7B. The majority of the addressable market is in the emerging markets in Latin America, the Middle East, Africa and Asia, together representing 90% of potential global subscribers of the industry. In terms of organizing the network connection of end users, the sector is divided into two parts: Direct-to-Premises (direct connection of households) and Wi-Fi Hotspot (organizing access through public Wi-Fi hotspots). In the forecast period (2018 – 2028), it is expected that Direct-to-Premises will provide 69% of revenue in comparison to 31% of Wi-Fi Hotspot. In terms of SV orbit, the Satcom market can be divided into GEO and non-GEO segments. At the same time, pursuing the objective of reducing the cost of services, operators (in both orbits) are switching to HTS satellites.

Advantages of non-GEO constellations broadband communications when compared to GEO SV:

- Significantly lower cost of putting a SV into orbit

- Significantly lesser data latency

- Ability to cover circumpolar regions

- Significantly lower cost of a satellite and much shorter production cycle

Disadvantages of non-GEO constellations broadband communications when compared to GEO SV:

- Business model has yet to prove its validity

- Provision of services cannot be started using one satellite – a large SV fleet is needed

- Ground segment (consumer terminals) is much more complex and expensive

The satellite broadband market has traditionally been served by GEO satellites. It is estimated that the sector will continue to be in the lead and have about 89% of the total revenue in the forecast period. So far, streaming video (social networks, YouTube) is the largest bandwidth consumer and will increase exponentially over the long term. The limitations on the allowed volume of data (for many satellite Internet packages) are still too low to support streaming for several hours per day. Consequently, a satellite cannot attract the main consumer, thus resulting in a slow growth rate.

Consumer Broadband Market drivers:

- Demand for traffic per person is growing

- Growing competition leading to lower prices for Internet access services

- Increasing number of developing countries entering the consumer market.

The high cost of services and equipment, as well as throughput limitations, are two main constraints to the spread of satellite broadband Internet access. There are two leading operators in the Consumer Broadband sector: ViaSat and EchoStar (through HughesNet, a subsidiary). These two companies are monopolists in the North American market (with a total of about 2 million subscribers, which is 74% of the total number of connected subscribers in the world).

1. Basic concepts and background

Satellite Internet access is Internet access through communications satellites, usually provided to individual users through GEO satellites. The development of the K frequency band (Ku, Ka) was a significant improvement in satellite Internet. The utilization of the frequencies commenced in 1993 and led to a vast increase in the throughput of satellites.

In 2004, with the launch of the first high throughput satellite (HTS) Anik F2, the next-generation class of satellites was put in service, providing improved throughput and bandwidth.

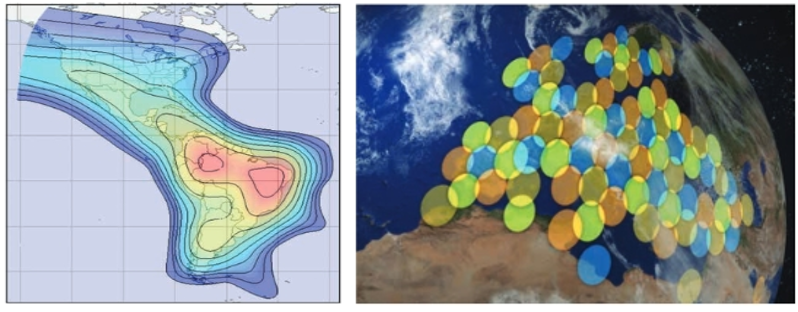

HTS satellites are designed and optimized for broadband applications involving multiple narrow-band beams targeting a much smaller area than the wide beams used by earlier communications satellites. This spot beam technology allows satellites to reuse the assigned bandwidth, enabling them to achieve much higher overall throughput than one of the conventional broadband satellites. Spot beams can also increase performance and respective capacity by focusing more power and increased sensitivity of the receiver in specific focused areas.

The difference between conventional satellite and HTS approach is schematically shown below (conventional GEO satellite coverage map is on the left, HTS satellite – on the right)

So that a connection is classified as a broadband one, it should meet the minimum data rate requirements of 25 Mbps for downlink and 3 Mbps for uplink (the speeds, which classify satellite Internet as a broadband one according to the FCC (Federal Communications Commission)). With the emergence of HTS satellites, one may say that satellite Internet has become broadband.

The consumer satellite Internet is now (mainly) a means of last resort (it is used as a last resort if other solutions are unavailable), and its main consumers are residents of remote or sparsely populated areas (where the deployment of terrestrial networks is not economically feasible). This type of Internet access is also a non-alternative option for connecting on an aircraft or a ship. The main advantage of satellite Internet is the ubiquitous availability of Internet access (to circumpolar regions, as regards GEO satellites).

Satellite internet has a number of disadvantages:

- High cost of services (the cost of services provided through terrestrial broadband networks is currently lower). High cost of services is complemented by high cost of ground equipment that the consumer should install at home (the average purchase price of consumer equipment in the EU is 350 euros (source)).

- Circumpolar regions are not covered (GEO orbit is not visible starting from 79 degrees latitude). The higher the latitude is, the lower percentage of GEO orbit is visible from the surface, and consequently the fewer number of available satellites.

- Signal latency associated with great distances (together with the delays in the ground switching centers, the latency can last 2 – 4 seconds) imposes limits on the applications used (inappropriate for online games, video communications).

- Decrease in the signal and its complete absence in a situation when the Sun and a satellite are in line with the receiving antenna (the Sun behind the satellite position). In the middle latitudes of the Northern Hemisphere, sun interference occurs from February 22 to March 11 and from October 3 to October 21, with a maximum duration of up to ten minutes.

- Exposure to moisture and various forms of precipitation (such as rain or snow) along the signal path between end users or ground stations and the satellite used. The effects are less pronounced for L and C low-frequency ranges, but can become quite strong for Ku and Ka high-frequency ranges. For satellite Internet services in tropical areas with heavy rainfall, C band (4/6 GHz) is commonly used. Ka band satellite communications (19/29 GHz) can apply adaptive power control of data transmission signals whenever there is precipitation to mitigate its negative impact.

- There are usually throughput limitations (or limitations on the allowed volume of data per month). It limits the use of satellite Internet for streaming video viewing – and this is currently the focus area for users.

The high cost of services and throughput limitations are two main constraints to the spread of consumer satellite Internet.

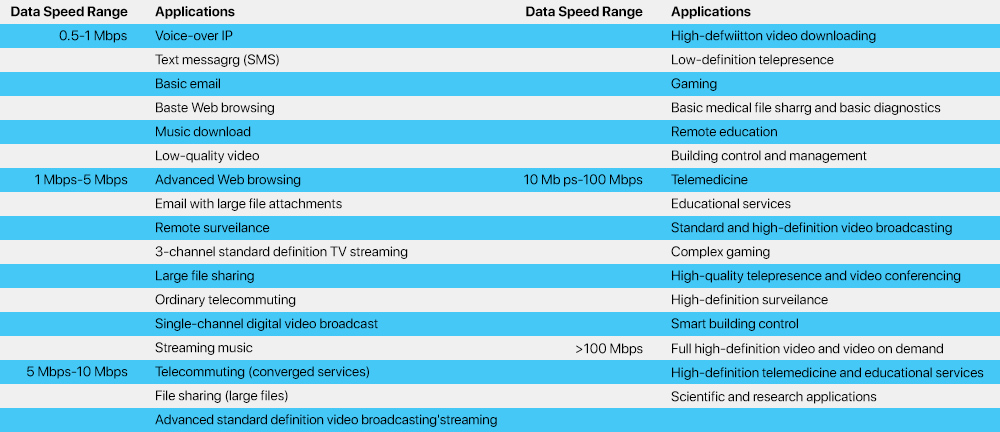

Below is the information on the available applications running at various bandwidth levels.

1.1 Broadband Internet penetration in the USA, Europe and in global terms

In global terms

At this stage, the broadband Internet coverage ratio of 50% has been achieved in the world (half the population has Internet access), but a significant part of the population is still either not connected to the Internet (due to the lack of terrestrial networks in the region) or does not use it as the cost of accessing is significant (source).

The estimated broadband Internet market is about 433+ million of households, and the current Satcom market penetration is only 0.63%, which is equivalent to 2.7 million of consumers (of which 2 million are in the USA and served by two top players EchoStar and ViaSat).

The number of subscribers to satellite broadband Internet is expected to grow steadily. In this regard, the North American region will be in the lead (in terms of the number of subscribers), and the Asia region will show the greatest growth.

Europe

By the end of 2013, 100% of EU households had access to basic broadband Internet, this was achieved through (source):

- Fixed connection (ADSL, VDSL, cable, fiber), providing 96.1% access

- Mobile communications, 99.4% covered households

- Satellite communications, the level of accessibility has been brought up to 100%.

The share of households not covered by land + mobile networks was only 0.6%, which is equivalent to about 3 million households. Some member states successfully introduced a voucher scheme for connecting remote communities using satellite broadband communications. In accordance with such a scheme, a government agency provides financial support (a voucher) to appropriate end users, using which they can “pay” to the registered service provider of their choice for the purchase, installation, and activation of a satellite user equipment. The service provider is reimbursed for its expenses by the government agency implementing the scheme.

Projects in support of the development of satellite technologies in Europe:

- SABRE – an association of regional authorities and stakeholders to tackle the Digital Divide in EU-28 and to ensure broadband coverage for all.

- BRESAT – provides information on the broadband coverage by region, case studies of satellite broadband deployments, key criteria and best practices for successful deployments, potential sources of funding, cost-benefit analysis, guidelines for business case development as well as hosting workshops and dissemination events across Europe.

There are 148 satellites providing services to Europeans. Basic packages start at 10 euros per month, with packages of 20 Mbps from 25 euros per month, the average prices for satellite dishes are 350 euros (it can be cheaper with a premium subscription).

USA

At the end of 2016, approximately 98.1% of US residents had access to either fixed terrestrial communications at a speed of 25 Mbps / 3 Mbps or to mobile communications at a speed of 10 Mbps / 3 Mbps, though in rural areas the figure was 89.7% (source: fcc.com).

Nevertheless, more than 19 million Americans (6% of the population) still do not have access to fixed terrestrial broadband at a speed of 25Mbps / 3Mbps. In rural areas, almost one quarter of the population – 14.5 million people – does not have access to this service. In tribal areas, nearly one third of the population does not have access. Even in the areas where there is broadband, about 100 million Americans are still not connected. 19 million people (having no access to terrestrial networks) are regarded as 7.6 million households (assuming 2.5 people per household). To date, the number of subscribers is only 2 million households; therefore, the satellite Internet market penetration is only 26%.

The next generation of Hughes and Viasat satellites, Jupiter-3 and Viasat-3, respectively, are scheduled to be launched in 2021. After reaching the orbit, they will provide US consumers with more than 100 Mbps Internet speed – the same speed that terrestrial providers offer their customers in major cities (source). A rural broadband development program (Rural Digital Opportunity Fund) has been launched in the USA. Within the framework of the program, it is planned to allocate funding in the total amount of USD 20.4B within 10 years (source).

However, the FCC set a limit of 100 milliseconds or less latency, resulting in satellite operators be at a disadvantage (since even MEO satellites cannot provide such a latency) (source). In the latest FCC rural broadband program, Connect America Fund 2, amounting to USD 1.49B, ViaSat was the only satellite operator to receive any funding (USD 122M). Hughes Network Systems, ViaSat’s main competitor in the US satellite broadband market, refused to compete in a tender for funding Connect America in 2018 citing an objection to the evaluation criteria (source: spacenews.com).

2. Broadband satellite market forecast

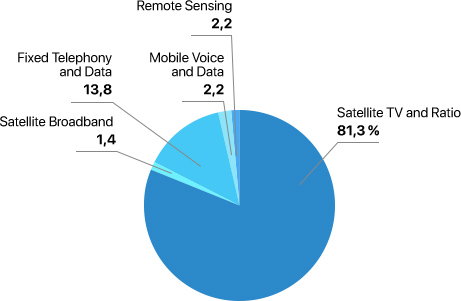

The broadband market is one of the Satcom market segments.

Satcom market shares by segments (for 2014)

Although the revenue from TV is still in the lead in the industry, the share of this sector has been declining over the past years, while noting an increase in the share of data transfer/broadband Internet (source).

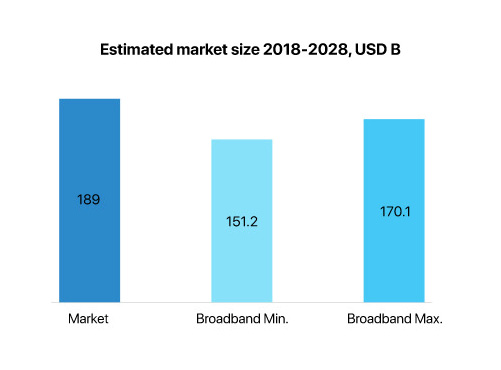

The satellite broadband market is growing and is forecast (for the period of 2018 – 2028) to reach a total volume of USD 189B (revenue from services and equipment). (source).

Historically, the revenue of SV operators and distributors (directly working with end users), in the structure of the market volume, amounted to 80 – 90% of the cost (source), accordingly the broadband market volume is USD 151.2 – 170.1B.

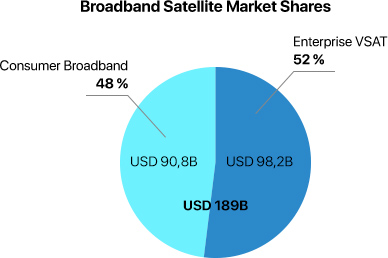

In general, and in terms of end users, the market is divided into two large sectors: Enterprise VSAT and Consumer Broadband.

2.1 Consumer Broadband

The Consumer Broadband segment is USD 90.8B (total revenue for 2018 – 2028 including services and equipment), and service revenue in this segment is expected to reach USD 79.7B (source).

According to analysts, there is great potential in the Consumer Broadband market segment, as despite the fact that the broadband Internet coverage ratio of 50% has been achieved in the world (half the population has the Internet access), a significant part of the population is still not connected to the Internet.

The majority of the addressable market is in the emerging markets in Latin America, the Middle East, Africa and Asia, together representing 90% of potential global subscribers (source).

The estimated broadband Internet market is about 433+ million of households, and the current Satcom market penetration is only 0.63%, which is equivalent to 2.7 million of consumers.

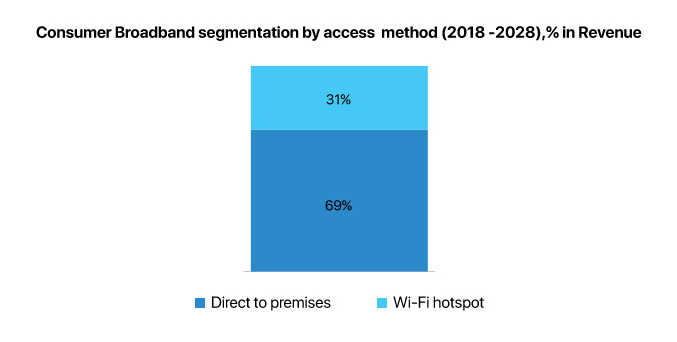

At the same time, in terms of organizing the network connection of end users, the sector is divided into two parts: Direct-to-Premises (direct connection of households) and Wi-Fi Hotspot (organizing access through public Wi-Fi hotspots) (source).

Numerous satellite communications market players are making offering of Wi-Fi hotspots to serve the lower segments of the market. The target market for such solutions is significant and mainly consists of the population in developing countries living in the areas poorly served by terrestrial networks.

The annual revenue from Wi-Fi hotspots services is forecast to reach USD 7.5B by 2027, which is 43% of the total revenue from satellite broadband services in 2027 (source).

In addition, there is a number of constraining factors in this segment:

- Income of the target audience is very low, therefore operators have to offer entry-level packages at minimal cost, and sometimes even free of charge (source).

- Availability of cheap and easily accessible electricity to power ground equipment.

- Availability of skills of networking and its use among the local population.

- Lack of necessary content, and therefore the Internet access demand.

In terms of SV orbit, the Satcom market can be divided into GEO and non-GEO segments. At the same time, pursuing the objective of reducing the cost of services, operators (in both orbits) are switching to HTS satellites (such satellites are characterized by high throughput and lower costs per bit of information compared to conventional satellites). 2/3 of the market is forecast to be generated by HTS satellites by 2028 (source).

The satellite broadband market has traditionally been served by GEO satellites. It is estimated that the sector will continue to be in the lead and have about 89% of the total revenue in the forecast period.

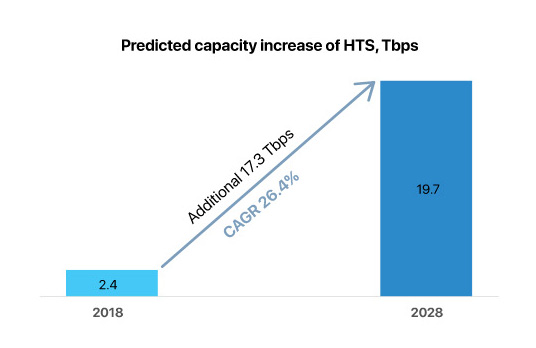

At the same time, the throughput of GEO-HTS is forecast to grow with CAGR of 26.4% over the next 10 years, approaching 20 Tbps by 2028.

So far, streaming video (social networks, YouTube) is the largest bandwidth consumer and will increase exponentially over the long term – streaming video that is, not linear TV (a sector that is expected to decrease) (source).

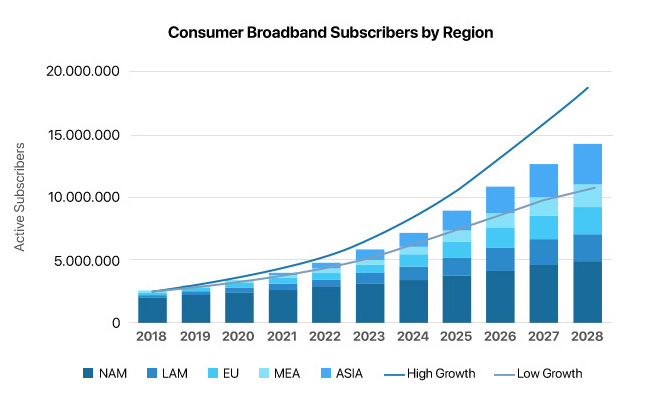

In global terms, the number of satellite broadband subscribers can reach 14 million subscribers by 2027 (source: NSR.com). These figures can be achieved only if Satcom could meet the expectations of subscribers with regard to higher volumes of data or with a higher resolution for streaming while reducing prices. The mid-level satellite Internet package is currently able to satisfy those users who generate traffic using a web browser and social networks; however, the limitations on data volume are still too low to support streaming for several hours per day. Consequently, a satellite cannot attract the main consumer, thus resulting in a slow growth rate.

The CISCO VNI 2017-2022 report states that IP video represents 75% of the total IP traffic, and the consumption profile for a satellite communications subscriber is not very different. Therefore, the ability to stream video is a major factor in determining the quality of services for satellite Internet subscribers.

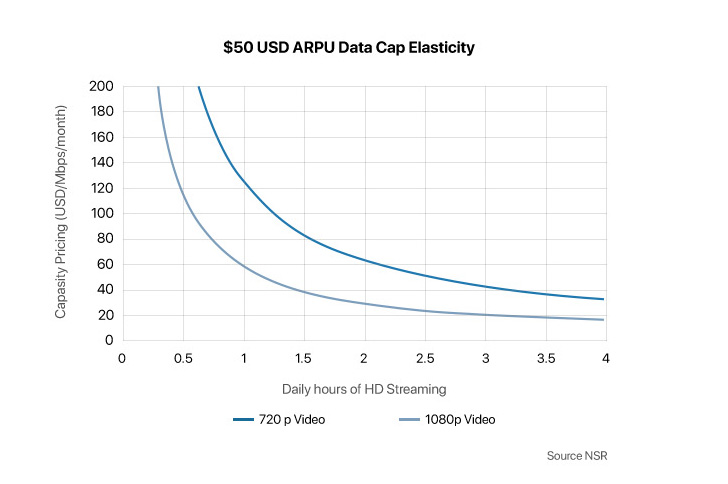

The prices of satellite throughput being USD 200/Mbps/month, the subscriber plan of USD 50 will be limited to ~ 10 GB, which is not enough to satisfy video-oriented users today. If the industry intends to unleash the potential of this market, the throughput prices should fall below the threshold of USD 100/Mbps/month, in which case the allowed volumes of data could increase considerably and improve the level of customers’ satisfaction (source: NSR.com). The dependence of the available time of video streaming at different levels of satellite bandwidth costs is given below.

Consumer Broadband Market drivers:

- Demand for traffic per person is growing and expected to reach 85 GB per user by 2022 (the global average), which corresponds to a threefold increase in demand over a five-year period (source: Spacenews.com).

- Growing competition leading to lower prices for Internet access services (which attracts more and more users). Currently, the cost of satellite throughput is about USD 200 – 300/Mbps/month, and further price reduction is expected (upon entering the market by mega LEO SV constellations, as well as in connection with the scheduled launch of VHTS satellites (Jupiter-3 and Viasat -3) by market leaders in 2021) (source: NSR.com).

- Increasing number of developing countries entering the consumer market.

The cost of services provision is still the main constraint on the Consumer Broadband market. If operators could reduce the cost to the level of the cost of terrestrial networks – this will have a significant impact on the market – it could lead to increased demand (driven by the interest of consumers from areas with developed infrastructure). So far, the main consumers are people living in hard-to-access regions (remote from urban areas).

3. Satcom and Consumer broadband market players

Currently, there are more than 50 satellite operators jointly operating 300 satellites in the GEO satellite segment. The sector is dominated by the four largest providers (Eutelsat, Inmarsat, Intelsat and SES), which in fact provide global coverage and together receive almost two-thirds of the Satcom market revenue.

SV operators use the capacities of their satellites themselves and sell (lease) them. It is expected that the lease revenue will decrease in the short- and medium-term due to the most recent renewal of SV fleet, which will replace outdated fleets of conventional FSS satellites based on both video and data pricing.

The revenue of service providers, on the contrary, will grow (due to the growth of the Consumer broadband, Maritime (connection of ships), and IFC (connection during flight) sectors).

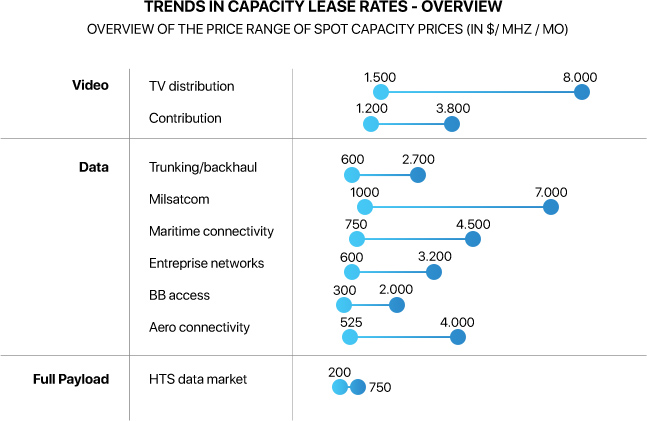

As of 2018, the level of prices for SV capacity lease was the following (source)

There are two leading operators in the broadband Internet sector: ViaSat and EchoStar (through HughesNet, a subsidiary). These two companies are monopolists in the North American market (with a total of about 2 million subscribers). While the number of globally connected subscribers was 2.7 million as of 2018.

3.1 Non-GEO Segment

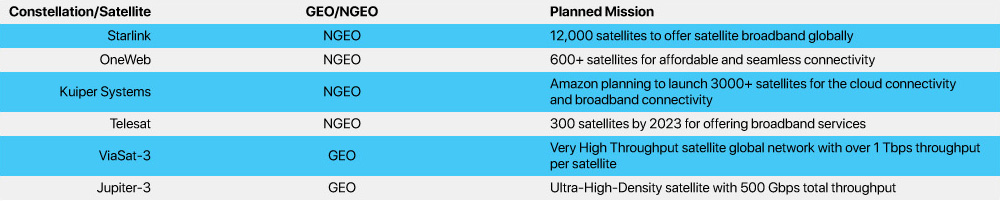

A number of players, which announced the deployment of large constellations of LEO/MEO SVs, are also seeking to enter this sector. Below is a comparison of the major broadband-oriented projects.

It should be noted that numerous ongoing programs (non-GEO) are facing latencies or were withdrawn from the market due to the financial crisis. Thus, Leosat, which was nurturing a plan of 78 – 108 satellites for high-speed Internet, abandoned the project as there were no investors.

Advantages of non-GEO constellations broadband communications when compared to GEO SV:

- Significantly lower cost of putting a SV into orbit (however, this is offset by the number of satellites needed to ensure global uninterrupted coverage).

- Significantly lesser data latency in comparison with GEO SV (as the orbit is much lower), which is critical for a number of applications.

- Ability to cover circumpolar regions (in case of polar orbits utilization).

- Significantly lower cost of a satellite and much shorter production cycle in comparison with GEO satellites. In this regard, financial losses due to the failure of one or more SVs or emergencies when entering into orbit are less significant.

Disadvantages of non-GEO constellations broadband communications when compared to GEO SV:

- Business model has yet to prove its validity.

- Provision of services cannot be started using one satellite – a large SV fleet (constellation) is needed to ensure uninterrupted communication and global coverage.

- Ground segment (consumer terminals) is much more complex and expensive than the one of GEO satellites. It has to do with the short time of one satellite visibility and the necessity to switch connection from one spacecraft to the next one, or simultaneous connection to several satellites. This can be accomplished using flat-panel antenna technology (a developing technology), the cost of such antennas is now several times higher than the cost of equipment for connecting to a GEO satellite. It is expected that it will take several years before the level of prices for such equipment be acceptable to consumers of broadband satellite communications (source: NSR.com).

3.2 Comparison of ViaSat and HughesNet (EchoStar)

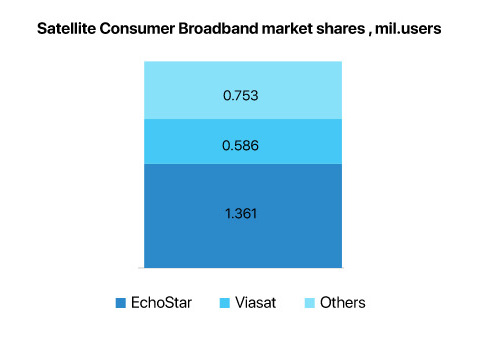

ViaSat (formerly Exede) and HughesNet (owned by EchoStar) are the two largest providers of satellite Internet for end users (households). Taken together, their share is about 74% of the number of global satellite Internet subscribers.

At some point, there were five alternative satellite Internet providers in the North American market. However, as a result of mergers/acquisitions and reorientation of some companies, only two leaders – HughesNet and ViaSat – remained in the industry and now share this market (source).

They both are widely available and use satellite technology in order to provide broadband Internet services.

EchoStar has more than twice as many subscribers as ViaSat, providing the company with 69% of the North American market. This large share of the market enables EchoStar to charge a lower price due to larger scale.

ViaSat has nearly 600 000 subscribers, but the company has lost customers after changing its strategy for entering the market. In recent years, ViaSat has moved to selling a larger number of premium services with higher speeds and higher prices.

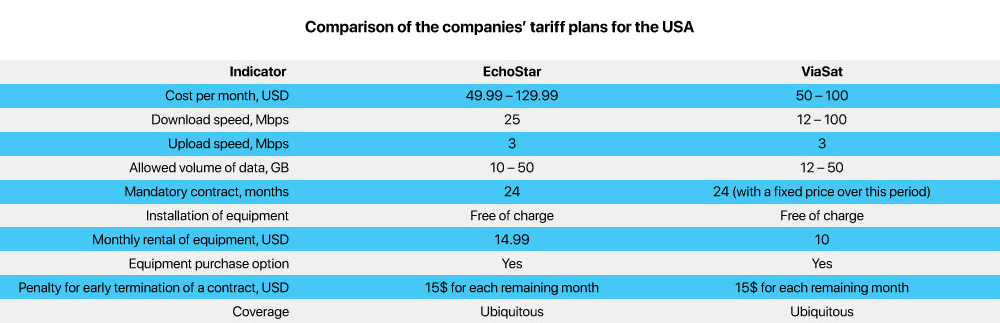

Both companies offer minimum plans starting from USD 50, EchoStar, however, having twice the speed of ViaSat, and premium ViaSat packages providing four times higher speed than its competitor. More detailed comparison of tariff plans is available here.

Both companies plan to launch new GEO satellites (Jupiter-3 and ViaSat-3) in 2021, which will increase their throughput significantly.

HughesNet is also an investor in OneWeb and has already been supplying them with satellite technology. HughesNet states that it will also provide ground systems, thereby ensuring access to the Internet through OneWeb constellation (source: factcompany.com).

Furthermore, on October 25, 2019, EchoStar completed the acquisition of Helios Wire for an undisclosed amount (source). By taking that step, EchoStar is expanding its satellite services beyond satellite communications, adding the Internet of Things (IoT) support, while gaining worldwide rights to the part of the S-band spectrum in which IoT networks operate.